Audit Sample Size for Small Population

Thus for the case above a sample size of. The relationship of the sample to the relevant audit objective.

2

05 The sufficiency of audit evidence is related to the design and size of an audit sample among other factors.

. According to the AICPA in SAS No. The size of a sample necessary to provide. Examiners should contact the Economic and Policy Analysis Division of the OCCs Economics Department for assistance in using statistical sampling for populations with fewer than 100 items.

Sample Size 133. When was the last time you examined 259 POs in an audit. See AS 2101 Audit Planning.

Randomisation and sample size for clinical audit on infection control J Hosp Infect. Refer to the table provided in the confidence level section for z scores of a range of confidence levels. Exceptions the sample size is 48 or 23 respectively for 5 and 10 percent exception rates which is rounded to 50 and 25 below.

16 When planning a particular sample for a substantive test of details the auditor should consider. 122 AU-C Section 530 audit sampling is defined as The selection and evaluation of less than 100 percent of the population of audit relevance such that the auditor expects the items selected the sample to be representative of the population and thus likely to provide a reasonable basis for conclusions about the. Remember that z for a 95 confidence level is 196.

Taking larger size samples 2. For purposes of the ISAs the following terms have the meanings attributed below. Sample Size is calculated using the formula given below.

The minimum sample size is 100. If you were taking a random sample of people across the UK then your population size would be just over 68 million as of 09 August 2021. The OCC uses a population size of 100 as a rule of thumb for the statistical sampling methodologies discussed in this booklet.

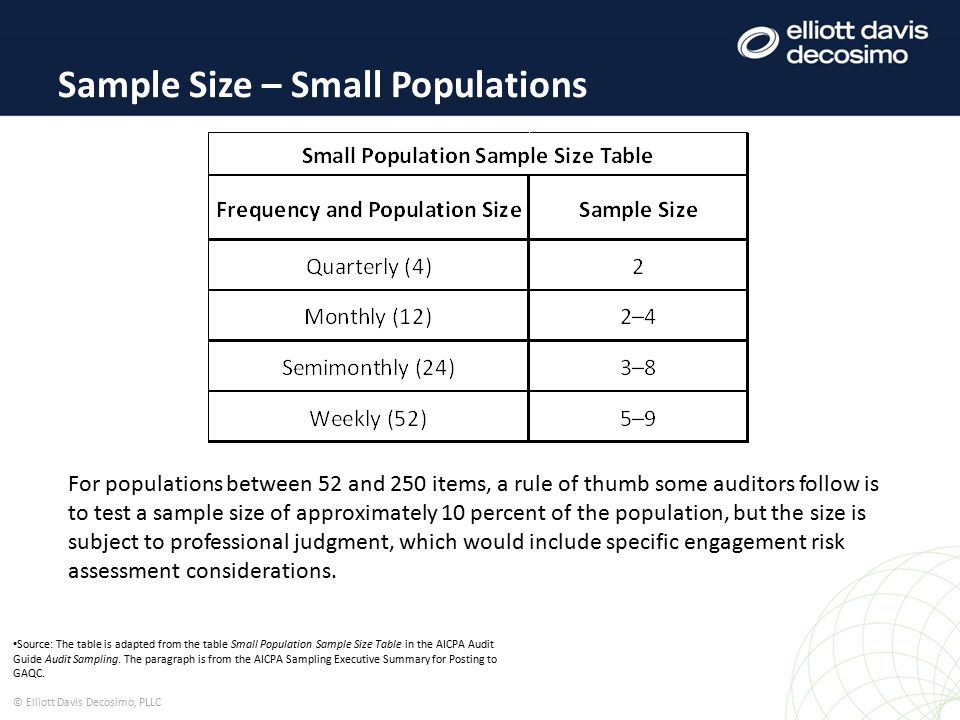

A Audit sampling sampling The application of audit procedures to less than 100 of items within a population of audit relevance such. Audit risk in turn is made up of two components the risk that a procedure is not effective and sampling risk. For populations between 52 and 250 items a rule of thumb some auditors follow is to test a sample size of approximately 10 percent of the population but the size is subject to professional judgment which would include specific engagement risk assessment considerations.

It is frequently performed on a proportion of the target population. However for a statistically valid audit sample for a 95 confidence level and a nonconformity rate of 1 or less you would have to sample 259 orders or a 26 sample. Most statisticians agree that the minimum sample size to get any kind of meaningful result is 100.

Audit Sampling 645 Sample Design Size and Selection of Items for Testing Sample Design Ref. Defining this group too narrowly will not give the best overall picture of those items most directly involved in the audit. If your population is less.

15 Planning involves developing a strategy for conducting an audit of financial statements. 5 rows the size of the sample is small when compared to the size of the population. Using random sample selection methods 3.

The auditor should. Surveys where you plan to use fancy statistics to analyse the results such as multivariate analysis if you know how to do such fancy statistics then you should already know how to choose a sample size. S small S 1 S 1 N.

For a population of 100000 this will be 383 for 1000000 its 384. Determine sample size controls - suggested minimum sample sizes 15 Significance of Control and Inherent Risk IR of Compliance Requirement Minimum Sample Size 0 deviations expected Very Significant and Higher IR 60 Very Significant and Limited IR Or Moderately Significant and Higher IR 40 Moderately Significant and Limited IR 25 Suggested minimum sample sizes for. The population is the group most important in any audit or research.

Similarly using 95 percent confidence zero exceptions and a 5 or 10 percent tolerable exception rate the sample size is 64 or 32 which is rounded to 65 and 35 below. In a hospital infec. In general factors that may lessen sampling risk include.

Epub 2010 Aug 6. Assume a population proportion of 05 and unlimited population size. Compliance sample size table Importancesignificance of Confidence Tolerable.

Standard deviation This refers to how much individual responses will vary between each other and the mean. Reasonable basis for the auditor to draw conclusions about the population from which the sample is selected. Populations must be defined to know and understand exactly who and what are being studied.

The auditor should determine that the population from which he draws the sample is appropriate for the specific audit objective. If you have a smaller population you will have to make an estimation of your population try to define your target group the best you can. Sampling risk is the probability that the sample results are not representative of the entire population.

Generalize from the sample to population. When designing the size and structure of an audit sample Auditors should consider the specific audit objectives the nature of the population and the sampling and selection methods. Small population sample size table Frequency and Population Size Minimum Sample Size Quarterly or 4 items 2 items Monthly or 12 items 2 to 4 items Semimonthly or 24 items 3 to 8 items Weekly or 52 items 5 to 9 items 52 to 250 items 10 of population Small populations are defined as populations of fewer than 250 items 21.

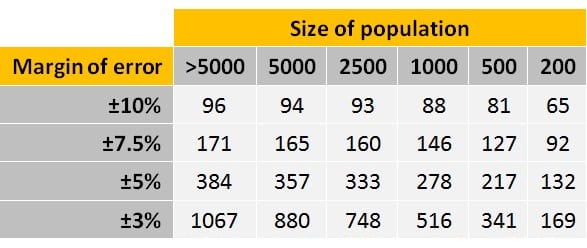

For example for a population of 10000 your sample size will be 370 for confidence level 95 and margin of erro 5. For example an auditor. Too broad a population will dilute the group.

The following sections explain what tools you can use and adjustments you can make to reach an unqualified report. The sample should represent the source population and be sufficient for statistical analysis. Following last years audit Audit firms use the same types of criteria to set an audits confidence level firm policy population size results of analytical review and other known facts about the client and its business.

Developing A Sound Sampling Methodology C Elliott Davis Decosimo Pllc Melody Reed Crcm Cfsa March 9 Ppt Download

How To Choose A Sample Size For The Statistically Challenged Tools4dev

What Is Sample Size Definition Omniconvert

Comments

Post a Comment